Cash vs Accrual Accounting: Which is Right for Your Business?

Have you ever thought about how companies keep track of their money? It looks easy, doesn’t it? But how you keep track of your money can have a big effect on how well your business does. The way you keep track of your income and expenses is more important than you might think, whether you own a small business or a big corporation.

There are two main ways to do accounting: cash basis and accrual basis. How you prepare your financial statements, how you report your taxes, and how you evaluate the health of your business all depend on each method.

In this article, we’ll talk about the differences between these two ways of keeping books and why picking the right one could change everything from how you handle your cash flow to how much you owe in taxes.

Key Takeaways: Quick Summary

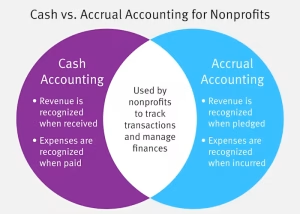

- Cash accounting: Tracks income and expenses when money changes hands. It’s easy and clear.

- Accrual accounting: Tracks income and expenses when they happen, not when the money is received or paid.

- Cash accounting: Best for small businesses with simple transactions because it makes tracking money easier.

- Accrual accounting: Best for big businesses or businesses with long-term contracts, lots of inventory, or complex financial transactions because it gives a more accurate picture of financial health.

What is Cash Accounting?

Definition

When cash changes hands, businesses that use cash accounting only write down their income and expenses. This means that you only write down your income when you get paid and your expenses when you pay them. It’s a quick and easy way to keep track of your money, so it’s great for businesses that don’t have to deal with complicated transactions or a lot of inventory.

Example

You work for yourself and send a client a bill for $1,000 at the end of the month. But the customer doesn’t pay until next month. You wouldn’t count that $1,000 as income until you got the money if you used cash accounting. This method works great for businesses that have a steady and simple cash flow.

Who Uses It?

Cash accounting is most often used by small businesses, sole proprietors, freelancers, and new businesses that don’t have a lot of complicated financial transactions. It’s also popular with businesses that don’t have a lot of stock or that provide services where customers usually pay right away after the service is done.

Benefits of Cash Accounting

- Simplicity and Ease of Use: Cash accounting is simple to use and requires minimal paperwork. Many small business owners find it easy to handle their money.

- Focus on Current Cash Flow: This method only records transactions when money changes hands, so you can see exactly how much cash you have right now. This helps in making quick decisions.

- Tax Benefits: Businesses can wait until they actually receive the money before paying taxes, which can be a big help with tax planning.

Limitations

- Cash accounting doesn’t show future income or expenses until they are paid or received, so it might not give a complete picture of financial health. This can hinder growth or funding opportunities.

- Not ideal for businesses with long-term contracts or lots of stock. Businesses with inventory or subscription-based services may not get an accurate picture of profitability. In these cases, accrual accounting is usually the better option.

What is Accrual Accounting?

Definition

Accrual accounting records transactions when they are earned or incurred, not when cash is exchanged. This method aligns revenue with the expenses that were incurred to generate that revenue, regardless of whether payment has been made or received. It provides a more comprehensive view of a business’s financial performance over time.

Example

Let’s say you run a marketing agency. You complete a project for a client in December, and the client agrees to pay $5,000 for the work. However, the client doesn’t pay until January. With accrual accounting, you record the $5,000 of revenue in December when the service was provided, not when the payment is received. This ensures that your income matches the period in which it was earned, providing a more accurate financial snapshot for December.

Key Differences Between Cash and Accrual Accounting

Timing of Revenue and Expense Recognition

Cash Accounting: Cash accounting means that you only record income and expenses when you get or pay cash. This means that transactions are recorded when the money actually changes hands, which gives a direct picture of cash flow.

Accrual Accounting: Accrual accounting means that money coming in and going out is recorded when the transaction happens, even if the cash isn’t exchanged right away. This ensures income and expenses are recorded in the same period as when they were earned or spent, giving a better picture of financial performance.

Complexity

Cash Accounting: Easy to understand and use, great for small businesses or individuals with simple transactions. No extensive accounting knowledge is needed.

Accrual Accounting: More complex and requires robust systems to track income and expenses accurately. Involves deferred revenue, prepaid expenses, and accrued liabilities. Best for larger companies with more complicated finances.

Adherence to the Matching Principle

Cash Accounting: The matching principle doesn’t apply because transactions are recorded when cash changes hands, which may misrepresent the business’s performance for a specific period.

Accrual Accounting: The matching principle ensures income and expenses are recorded simultaneously, providing a more accurate picture of profitability over time.

Use of Accounts Payable/Receivable

Cash Accounting: No accounts payable or receivable; transactions are only recorded when cash is exchanged. Money billed but not received isn’t considered an asset.

Accrual Accounting: Tracks accounts payable (money owed to suppliers) and accounts receivable (money owed by clients), giving a complete view of financial health even if cash hasn’t changed hands yet.

When to Use Cash vs. Accrual Accounting

Small, Simple Businesses

Cash accounting is ideal for small businesses without credit or inventory, such as freelancers or small shops. Transactions are straightforward, and cash flow is easy to track.

Growing Businesses

Accrual accounting is better for businesses with long-term contracts, inventory, or complex transactions. It matches revenues with costs, providing a clearer picture of profitability and future obligations.

Regulatory Requirements

If your business earns more than $25 million annually, the IRS requires accrual accounting. Businesses below this threshold can use cash accounting, though accrual may still be preferable for inventory or credit-based purchases.

How Cash and Accrual Accounting Affect Financial Reporting

Short-Term Profitability vs. Long-Term Accuracy

Cash accounting can make short-term profits appear higher because income is recorded only when cash is received. Accrual accounting provides a more accurate picture by matching revenues with expenses in the same period.

Cash Flow Management

Cash accounting gives a direct view of real cash flow, crucial for small businesses managing daily operations. Accrual accounting tracks long-term financial health but may make daily cash flow less visible.

Benefits of Cash Accounting in Real-Life Situations

For Solo Entrepreneurs

Cash accounting simplifies bookkeeping for freelancers or consultants. Income is recorded only when received, and expenses only when paid. It reduces stress by aligning financial records with actual cash in hand and makes tax filing easier.

When Cash Flow is Key

Ideal for small retail stores or businesses where daily cash flow is essential.

- Immediate Cash Flow Visibility: See cash on hand immediately after sales.

- Clear Budgeting: Know exactly how much money is available for daily expenses.

- Simplified Tax Filing: Income and expenses are recorded only when cash changes hands.

Example: A small store makes $500 in sales in one day. Cash accounting records the $500 immediately, giving an accurate view of available cash for operating costs.

How Each Method Affects Taxes

Cash Accounting

Taxes are paid only when income is received. Small businesses benefit from flexibility in managing when they pay taxes, especially if cash flow is inconsistent.

Accrual Accounting

Taxes are recorded when income is earned and expenses are incurred, even if cash hasn’t been received. This provides a clearer long-term picture but can be challenging for businesses with delayed payments.

What Steps Should You Take to Get Ready for Taxes?

Cash Accounting: Best for small businesses with simple transactions and limited inventory, allowing flexible recording of income and expenses for tax purposes.

Accrual Accounting: Helps larger or complex businesses plan taxes more accurately by recording income and expenses in the correct tax periods.

Hybrid Methods: Can You Use Both?

What Does It Mean to Do “Hybrid Accounting”?

Some businesses benefit from using both cash and accrual accounting. Accrual tracks inventory and complex transactions, while cash accounting tracks daily sales and immediate payments. This combination allows better cash flow control and accurate inventory management.

Example of Mixed Accounting

A small store uses accrual accounting for inventory management and cash accounting for daily sales and immediate expenses like wages or utilities. This approach simplifies tracking and financial planning.

Conclusion: Making the Right Choice

Cash Accounting

Simple and effective for small businesses with straightforward day-to-day transactions. Only tracks money when it changes hands, simplifying tax preparation.

Accrual Accounting

Better for larger businesses or those with complex transactions. Tracks income and expenses as they occur, giving a true picture of financial health.

Choosing the Best Option for Your Company

Consider your business size, complexity, inventory, and cash flow needs when deciding between cash and accrual accounting.

Final Decision

For new or small businesses, cash accounting is often the easiest. For growing businesses or those with complex transactions, accrual accounting provides a clearer long-term financial picture.

What are the costs of SG&A? All the information you need Copy

Have you ever thought about how companies keep track of their money? It looks easy, doesn’t it? But how you keep track of your money

What are the costs of SG&A? All the information you need

Understand SG&A Costs and Learn Where Your Money Really Goes You hear a lot about costs, profits, revenues, and margins when you run a business,

California Statement of Information: What It Is, Who Must File, and Why It Matters

California Statement of Information Running a business in California means following some key rules. One of those is filing a form called the California Statement